Welcome to Homeseed’s Mortgage Market Update, where we dive into the latest trends, insights, and changes shaping the dynamic landscape of the housing and lending industries.

Mortgage Rate Trends & Forecasts

Mortgage rates are higher this week as a result of strong labor market and manufacturing data.

The BLS Jobs Report showed nearly double the amount of jobs were added to the market than expected.

The ISM Non-Manufacturing PMI was also higher than expected and the upbeat economic data put additional upward pressure on rates.

BLS Jobs Report

The report for January showed that the 353,000 jobs created were nearly double the expected 180,000.

One thing to be mindful of is that January is a month of heavy adjustments due to new benchmarks, seasonal adjustments, and population controls.

Despite the job gains, the entire labor force is working on average 30 minutes less per week, which is equivalent to 2.4M jobs lost.

We will have to wait for February data to see if the labor market tightening once again.

Home Values Continue to Appreciate

The two most notable housing indices, Case-Shiller and FHFA, both recently released data showing that home prices set new highs.

Although data for December 2023 is not available yet, both indices show that home values were on pace to appreciate by 6% in 2023.

Lower numbers for existing inventory and active listings will continue to be supportive of home prices throughout 2024.

MEDIA SAYING HOUSING CRASH – But housing credit data today looks nothing like what was seen in 2008. https://www.housingwire.com/…

BOOST TO HOUSING SENTIMENT – The Fannie Mae Home Purchase Sentiment Index reached its highest level in nearly two years. https://www.fanniemae.com/…

TWO SIDES TO JOB MARKET – Economists and reports say the labor market is strong, but job seekers don’t share the same confidence. https://www.cnbc.com/…

Homeownership has long been considered a cornerstone of the American dream, providing not only a sense of stability and security but also a unique avenue for building wealth. For many, purchasing a home is not just about having a place to call their own; it’s a strategic financial move that can lead to long-term prosperity. Below we’ll provide a decade-by-decade analysis on home values and explore how homeownership is a powerful investment tool, enabling individuals to leverage their assets and capitalize on the appreciation of real estate.

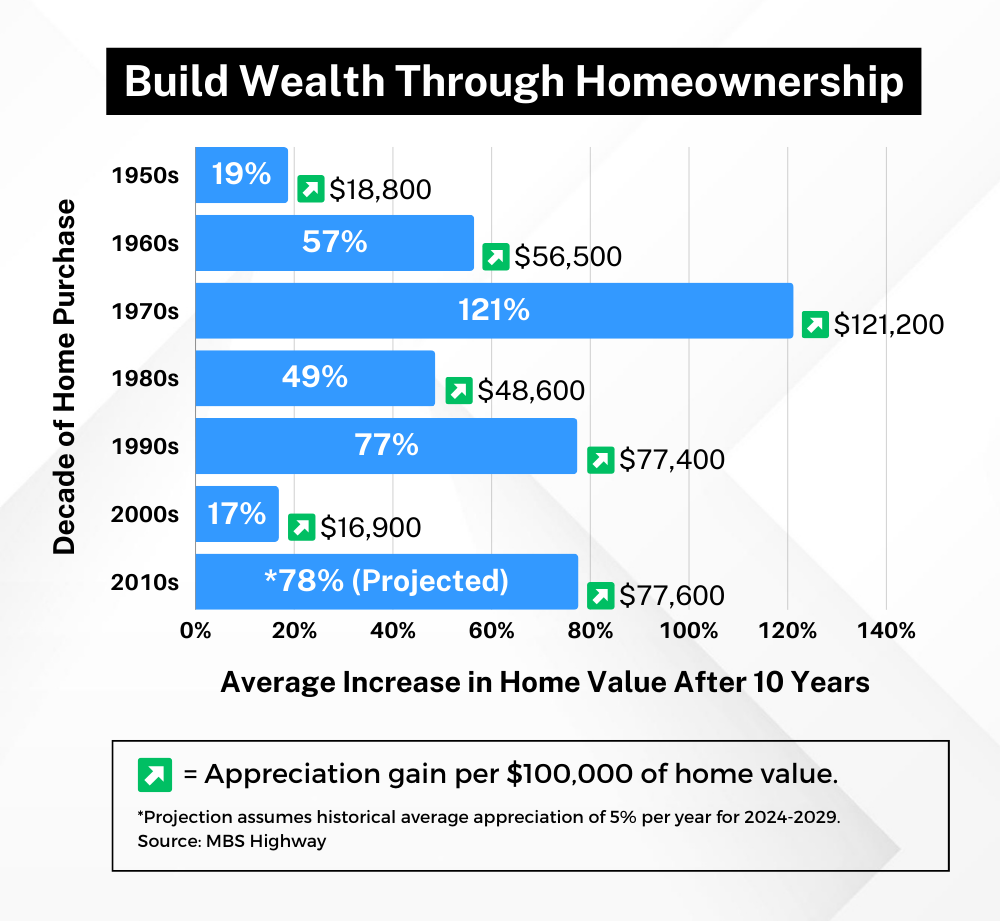

Historical Appreciation By The Decade

Consistent Appreciation: Regardless of the decade, those who invested in homeownership and held onto their properties for 10 years experienced positive appreciation on average. This consistency underscores the enduring nature of real estate as a wealth-building asset.

Diversification of Investments: The data highlights how real estate can serve as a valuable diversification tool for investment portfolios. While other assets may experience volatility, real estate has historically shown a trend of appreciation over time.

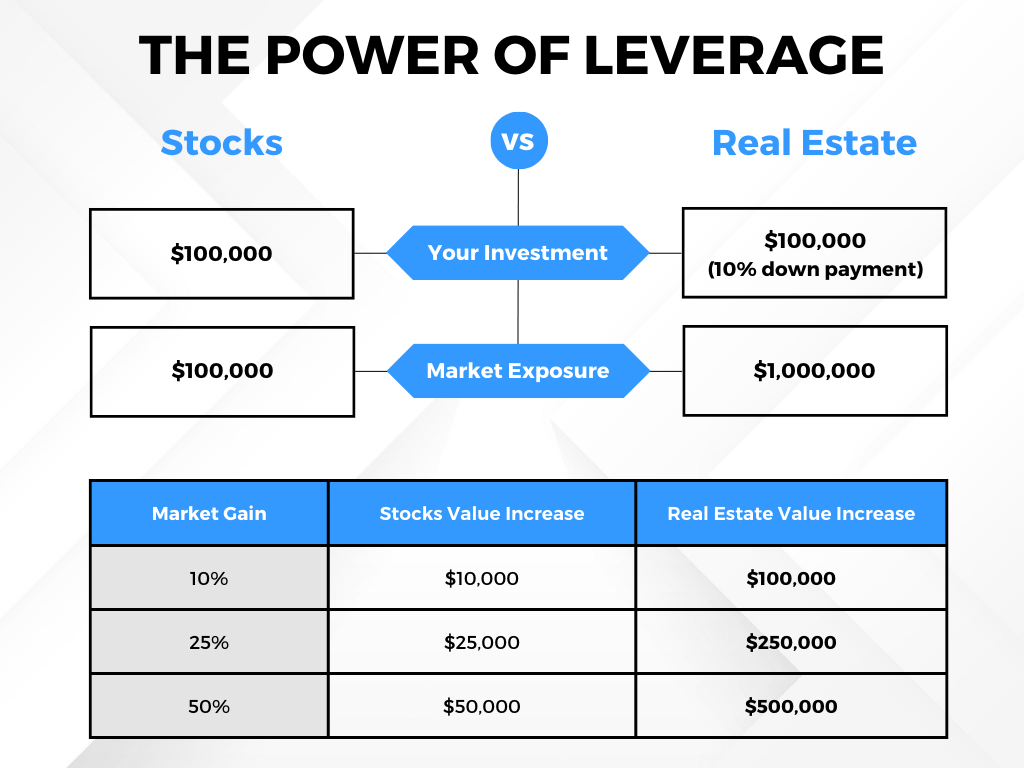

The Power of Leverage in Real Estate

One of the unique aspects of real estate investment is the ability to use leverage. When you purchase a home, you typically make a down payment (an initial investment) while borrowing the rest through a mortgage. This means you control an asset’s full value with a relatively small upfront payment. As the property appreciates, the return on your investment is calculated based on the property’s entire value, not just your down payment. This leverage magnifies the potential for wealth accumulation.

Homeseed Can Help You Get Started

Discover the possibilities with our exclusive loan programs that offer little to no down payment options. This means you can potentially start building equity and wealth with very little upfront investment. Our commitment is to make homeownership accessible and financially advantageous for you. Contact us today to discuss your goals, explore available opportunities, and make informed decisions about your real estate investment. Your path to homeownership and financial prosperity starts with a conversation. Let’s connect and turn your homeownership dreams into reality!

Welcome to Homeseed’s Mortgage Market Update, where we dive into the latest trends, insights, and changes shaping the dynamic landscape of the housing and lending industries.

Mortgage Rate Trends & Forecasts

Mortgage rates are relatively unchanged week-over-week with some volatility mixed in due to economic data and bond auction results.

Last week saw 2-year, 5-year, and 7-year Treasury auctions that were met with weak demand and put upward pressure on mortgage rates.

Recent GDP and labor market reports came in stronger than expected and the Fed would like to see more economic weakness to support disinflation.

Personal Consumption Expenditures (PCE)

Headline inflation rose 0.17% in January, close to the expected 0.2%, while the year-over-year reading remained at 2.6%.

Annualized core PCE over the last 6 and 8 months is 1.85% and 2.08%, respectively, which are close to the Fed’s target of 2%.

Although the Fed prefers the Core PCE measure for gauging inflation, it should be noted that the CPI tends to move the markets a bit more.

Pending Home Sales

Pending Home Sales (signed contracts on existing homes) surged 8.3% from November to December.

The large jump was attributed to the decline in mortgage rates we’ve seen since the highs back in October 2023.

The Chief Economist at the National Association of Realtors, Lawrence Yun, noted that sales are expected to rise significantly in each of the next two years.

An increase in the supply of homes on the market will be essential to satisfying all of the demand that current exists.

RATES UNCHANGED WEEK-OVER-WEEK – Mortgage rates were volatile within a narrow range over the last week but are relatively unchanged. https://www.mortgagenewsdaily.com/…

ECONOMY BOOSTED BY NEW HOME SALES – Continue demand for new housing helped employ workers, stimulate the purchase of goods, and avoid a recession in 2023. https://www.housingwire.com/…

ACTIVE INVENTORY RISES – For the 11th straight week, active listings grew and looks to improve availability and affordability heading into the spring season. https://www.calculatedriskblog.com/…

INFLATION CONTINUING TO COOL – The recent PCE report showed inflation continuing to cool and near the Fed’s 2% target. https://www.cnbc.com/…

At some point in our lives, we’ve all pondered the age-old question: when is the ideal moment to embark on the journey of homeownership? This decision is often influenced by personal finances and life circumstances. Fortunately, for those with the desire and means, the current market offers an advantageous time to make the move into homeownership. Despite some headwinds like rising home prices and higher interest rates, the numerous benefits of purchasing now far outweigh these obstacles.

An Investment to Build Wealth:

Owning a home builds equity, but that takes time for the asset to grow. The earlier you can start the better. Remember, time in the market beats trying to time the market.

Mortgage payments contribute to your ownership stake, unlike rent payments that go into your landlord’s pocket.

In the future, your home equity becomes a powerful financial tool to be leveraged for other investments or major life expenses.

Property values historically trend upward, providing you one of the safest investments you can make.

Homeowners enjoy tax incentives, with tax-deductible mortgage interest payments.

An Opportunistic Time to Purchase Now:

Forecasts indicate an expected decline in mortgage rates in 2024, which will likely increase affordability and heighten competition on the limited supply of homes.

Purchasing now grants an advantage ahead of the projected surge in competition, while allowing you to capitalize on equity gains and refinance opportunities once rates drop.

The higher loan limits for 2024 contribute to an increase in affordability for you, especially in the earlier part of the year as home prices are expected to continue rising throughout 2024.

Homeseed’s Programs & Strategies for First-Time Homebuyers

Down Payment Assistance Programs: Programs designed to aid with down payment and closing costs, providing valuable financial support to ease the initial financial burden of purchasing a home.

Zero Down Payment Loans: Loan programs requiring no down payment, particularly beneficial for veterans (VA) or those residing in rural areas (USDA).

First-Time Homebuyer Programs: Loan programs with lower down payments and improved rates that are created for low- to moderate-income first-time homebuyers.

Seller Concessions: We offer financing strategies where the seller can help provide additional assistance to reduce the cash you need to close.

Choosing homeownership over renting is a strategic move that goes beyond the immediate advantages of financial investment. It’s a commitment to building wealth and securing long-term benefits for you and your family. With Homeseed’s support and specialized programs for first-time buyers, the path to homeownership becomes even more attainable. Take the next step with Homeseed and make the move towards homeownership today.

Welcome to Homeseed’s 2024 Mortgage & Real Estate Forecast! As we enter the exciting year of 2024, the anticipation and speculation surrounding the mortgage market and housing industry have prospective homebuyers carefully watching. In just the last three years, we’ve gone from seeing all-time low mortgage rates to some of the highest mortgage rates in the last two decades due to significant global events and economic shifts. To better understand what potentially lies ahead for this year, let’s dive into a forecast for the mortgage market and housing industry in 2024.

Inflation: The Driving Force for Mortgage Rates

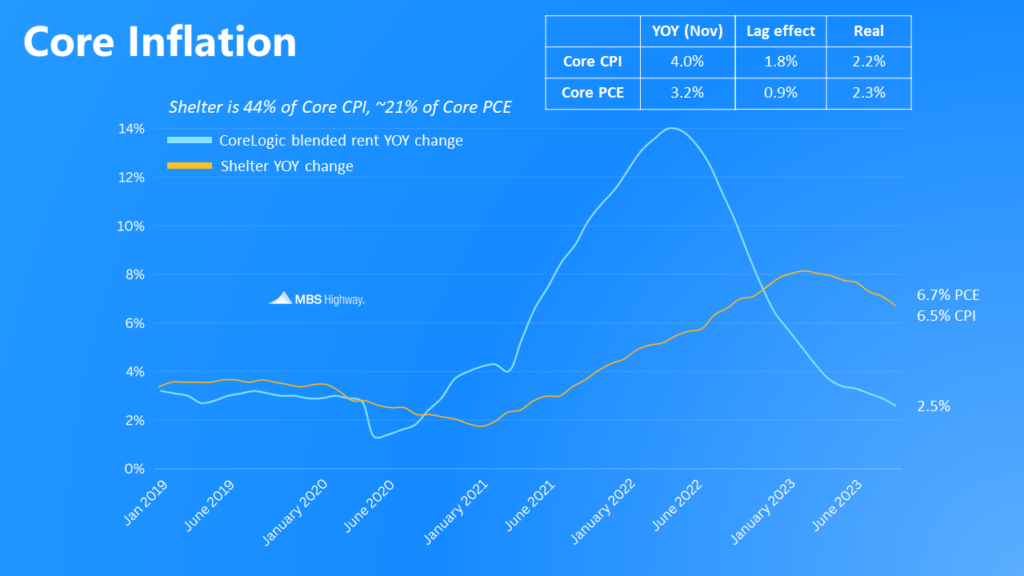

Inflation has emerged as a pivotal factor shaping the mortgage market. After reaching a near 40-year high of 5.3% in March 2022, Core Personal Consumption Expenditures (PCE) has been on a gradual decline and now hovers at 3.2%, which is near the Federal Reserve’s (Fed) goal of 2%. Given the improvement on inflation, the Fed signaled they would begin rate cuts to their Fed Funds Rate before reaching the 2% target in hopes of easing into its inflation goal with minimal negative effects to the economy. With shelter accounting for 21% of Core PCE, CoreLogic’s most recent measure of shelter costs showed a 2.5% year-over-year increase in their real-time blended rents data. This suggests a continued improvement for inflation lies ahead as the shelter data used by the PCE report lags the real-time shelter data, and the markets are now predicting the first rate cut by the Fed as early as March 2024.

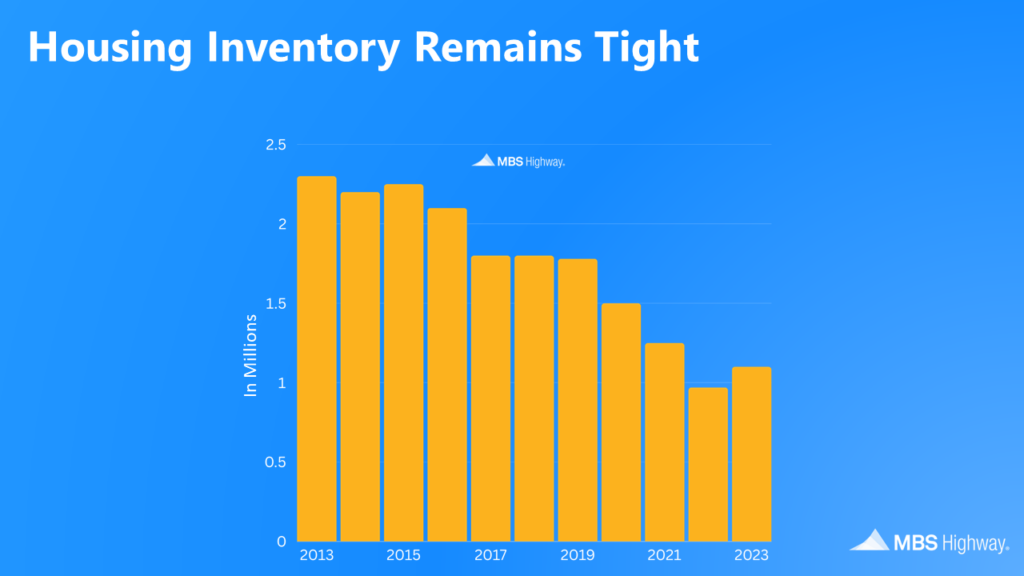

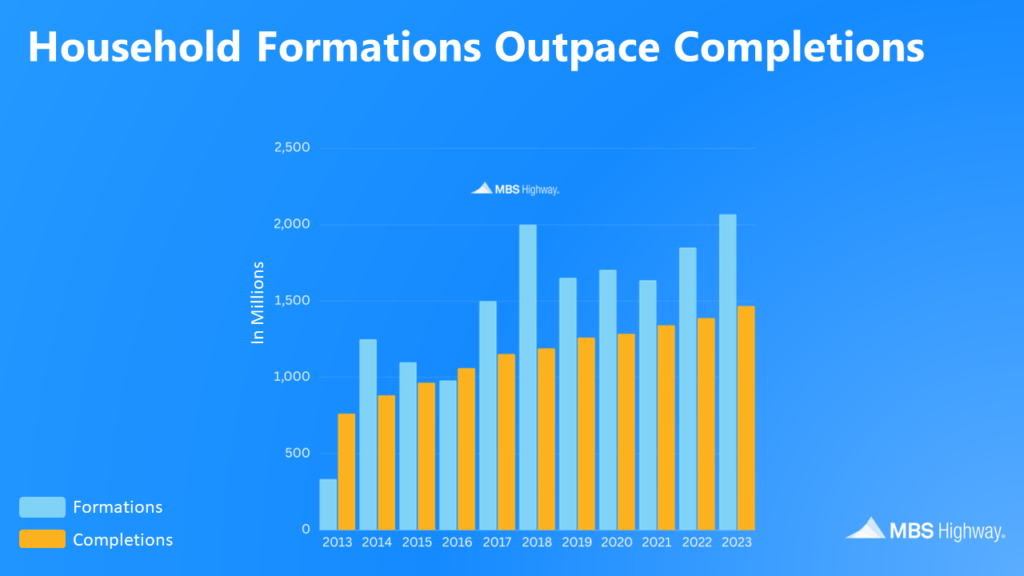

Supply and Demand: Limited Inventory Pushes Home Prices Higher

The housing market continues to grapple with enduring challenges in inventory shortage, fueling a steady increase in home prices. Despite efforts to address the housing deficit, housing starts persist below household formations, indicating a sustained scarcity of available homes for sale coming to the market that is unable to meet the escalating demand. This ongoing imbalance between the supply of homes and demand from buyers will likely intensify competition if mortgage rates continue to come down, leading to the possibility of bidding wars and soaring prices once again.

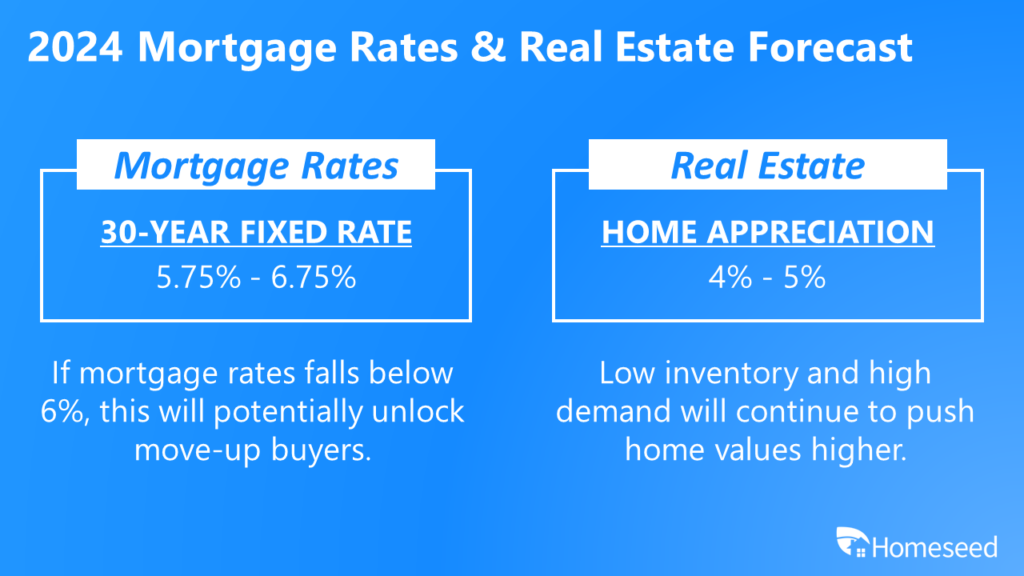

Mortgage Rate and Real Estate Forecasts

Given the trajectory of inflation, we forecast the 30-Year Fixed Rate Mortgage to fluctuate between a rate range of 5.75%-6.75% throughout 2024. If rates fall below 6%, this will potentially unlock move-up buyers who are current homeowners that want to upgrade their homes.

For home price appreciation, we forecast home values to increase between 4-5% in 2024. Values should stay strong as demand will remain high due to more households being formed than homes coming to market.

Seizing the Opportunity: A Time for Homeownership to Build Wealth

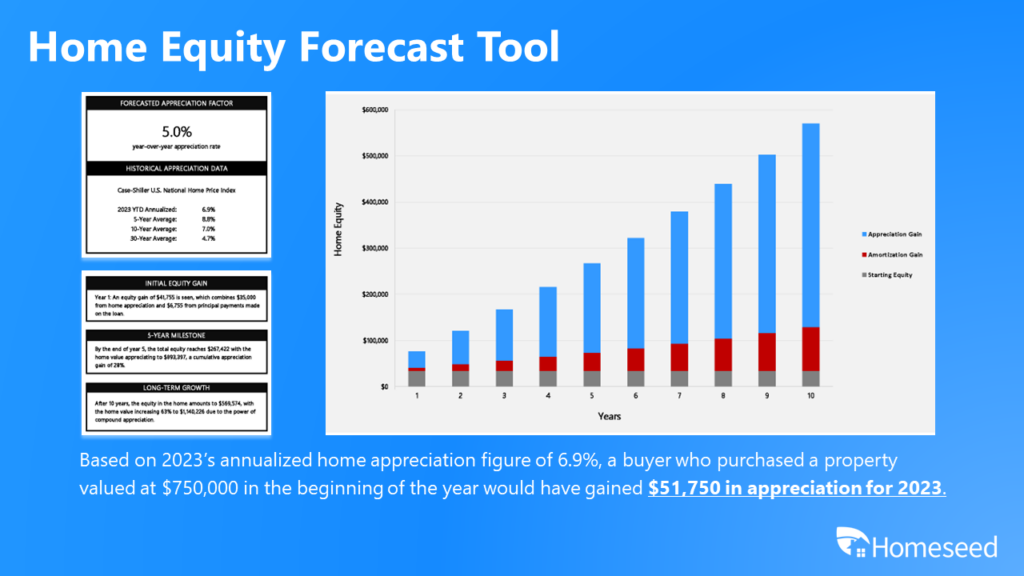

As we navigate the intricacies of 2024, this period stands as an opportunistic time for prospective homebuyers. With the likelihood of interest rates coming down and home prices on a continued ascent, buyers can consider the strategic move of securing a home now and later benefiting from potential refinancing opportunities in the near future. Here at Homeseed, we offer a Home Equity Forecast tool, shedding light on the significant wealth-building potential through home appreciation and amortization. It emphasizes that homeownership is not merely about costs and interest rates but extends to the concept of a home evolving into one of your most substantial investments for building wealth.

Welcome to Homeseed’s Mortgage Market Update, where we dive into the latest trends, insights, and changes shaping the dynamic landscape of the housing and lending industries.

Mortgage Rate Trends & Forecasts

Mortgage rates move lower once again this week with the biggest improvement happening yesterday after the Fed Meeting.

The improvement in rates were due to the Fed signaling that they plan to cut rates multiple times in 2024.

This week’s Consumer Price Index and Producer Price Index also showed inflation moving lower.

This Week’s Fed Meeting

The Federal Reserve had their last meeting of 2023 yesterday and maintained its benchmark Fed Funds Rate, opting to not raise or cut rates.

The big improvement in mortgage rates occurred when the Fed signaled it will likely cut rates by 0.75% in the year ahead, which is an increase of 0.25% from their previous meeting in September.

Remember, the Fed Funds Rate does not directly impact mortgage rates but this shift in outlook directly affects the bond market that mortgage rates are tied to.

CPI and PPI Inflation Reports

This was a good week for inflation news as many reports and forecasts showed inflation moving lower.

Tuesday’s release of the Consumer Price Index (CPI) report showed inflation moving lower year-over-year from 3.2% to 3.1%.

Yesterday’s Producer Price Index (PPI) report showed producer inflation falling from 1.2% to 0.9% year-over-year.

The Fed also announced yesterday that they also project inflation will fall to 2.4% in 2024, which is better than the 2.5% they projected in September.

GOOD NEWS FOR MORTGAGE RATES – Mortgage rates moved to the lowest levels since May with the help of some good news coming from the Fed yesterday. https://www.mortgagenewsdaily.com/…

FED MEETING RECAP – The Fed had their final meeting of the year and signaled rates cuts and a lower inflation prediction for 2024. https://www.yahoo.com/…

LARGE INCREASE IN MORTGAGE ACTIVITY – The Mortgage Bankers Association said that mortgage application volume was up 7.4% last week as rates continue to move lower. https://www.eyeonhousing.org/…

CONSUMER PRICE INDEX – The CPI for November showed inflation falling further to 3.1% compared to the pandemic-era peak of 9.1% in June of 2022. https://www.cnbc.com/…

Entrepreneurship offers numerous advantages, such as the exhilarating experience of building a business from scratch. However, many self-employed individuals are concerned the path to homeownership can present unique challenges compared to those with traditional employment since the nature of owning a business often leads to irregular income patterns and varied documentation. While that can be true in some cases, lenders will still be considering the same factors for a mortgage approval as any other type of borrower: your credit score, debt, assets, and income.

What Documents Do You Need To Provide?

Lenders need to ensure that a borrower can afford the loan they have applied for and will likely request the following documents from self-employed borrowers:

Last two years of filed personal tax returns

Last two years of filed business tax returns

Year-to-date profit and loss (P&L) statement

Evidence of your business existence

How Is Your Income Calculated?

Lenders will calculate your income by completing a cash-flow analysis from your last two years of tax returns and the income will be considered from various sources such as W-2, net business profits, K-1 earnings, and more. Let’s go over an example below:

Say your business earned $300,000 total in the last two years. If you had written off $180,000 in expenses in those two years, that would lower your net income down to $120,000. We would then divide your $120,000 net income by 24 months (two years) and qualify your monthly income at $5,000.

Please keep in mind that this is a very generalized example of how income is calculated and there are other factors that can impact qualification such as income stability, the location and nature of your business, the financial strength of your business, and the likelihood of you continuing to generate income in the future. We can also consider nonrecurring losses or expenses or depreciation, as a couple examples, to add back into income. In some cases, we only need to consider one-year of tax returns versus two-years.

Other Options For Self-Employed Borrowers

As a business owner, it’s understandable that you’d want to maximize your business deductions, which would result in a lower tax bill. However, showing low income on tax returns might not accurately represent the financial health or earning potential of the business. Homeseed recognized this issue and is also able to provide alternative solutions by offering unique loan programs such as Bank Statement loans, Profit and Loss (P&L) loans, and 1099 loans. These programs offer flexibility in income verification and cater specifically to self-employed individuals who may have non-traditional income documentation.

Bank Statement Loans: Bank statement loans are designed for self-employed borrowers who may not have consistent or easily verifiable income. Instead of tax returns, these loans consider bank statements over a specified period (often 12 to 24 months) to assess the borrower’s income. Lenders review regular deposits as income, thereby offering an alternative method for evaluating a self-employed individual’s financial stability.

Profit and Loss (P&L) Loans: P&L loans focus on the profitability of a business rather than personal income. These loans typically require the submission of profit and loss statements, business bank statements, and potentially other financial documents to assess the business’s overall health. This approach is beneficial for entrepreneurs who reinvest earnings into their business or pay themselves lower salaries for tax purposes. This loan type is also helpful when considering the timing of your purchase (for example, you have not filed current year’s taxes yet because the year is not complete, but you can provide a P&L statement to document current year-to-date income).

1099 Income Loan: Many freelancers, contractors, gig economy workers or other self-employed borrowers who file using W-9s cannot qualify for a mortgage under some Agency guidelines. Instead, these borrowers can use their 1099 earning statements in lieu of tax returns to qualify for a mortgage.

Tips for Self-Employed Borrowers

Self-employed borrowers face unique challenges in showcasing their income. This is especially important as we approach the end of the year and tax season approaches. Understanding the various methods of income calculation and different loan programs empowers individuals to prepare early for the mortgage process and purchasing a home. Seeking guidance from financial advisors or tax professionals will significantly aid in optimizing tax filings and accurately documenting income for loan applications as well.

Welcome to Homeseed’s Comprehensive Winter Mortgage Report, your guide to navigating the current landscape of the mortgage market and seizing opportunities in the real estate market! In this detailed report, we delve into crucial elements influencing the market, including the recently released 2024 loan limits, the impact of inflation and labor market dynamics, predictions regarding the trajectory of interest rates, insights into home values and appreciation trends, and most importantly, the window of opportunity awaiting potential buyers. Read on to equip yourself with essential knowledge for making informed decisions in the real estate sphere.

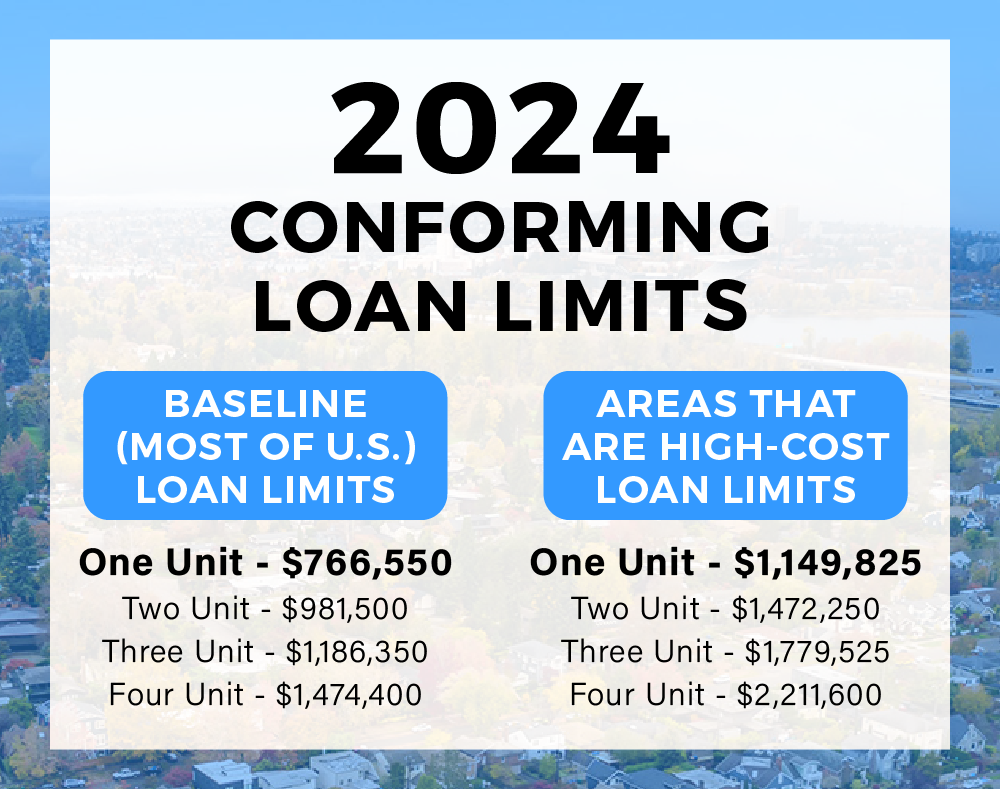

New Loan Limits

Annually, the Federal Housing Finance Agency (FHFA) sets conforming loan limits for the forthcoming year based on the November House Price Index (HPI), reflecting home price appreciation data. For 2024, the baseline conforming loan limit will rise to $766,550, marking a $40,350 increase from the 2023 limit of $726,200. This substantial increase aims to facilitate greater access to credit for home buyers in markets experiencing upward home price appreciation.

Inflation & Labor Market Data

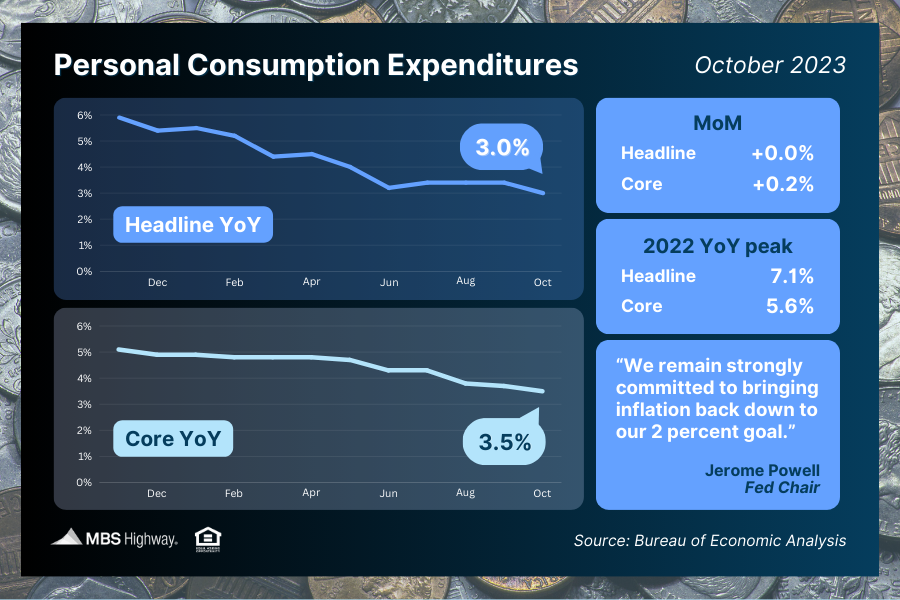

The recent softening in economic data and the labor market holds significance for the inflation outlook and its potential impact on mortgage rates. A weakened economic landscape tends to alleviate inflationary pressures as reduced consumer spending and constrained demand mitigate the upward push on prices. This was reflected in the Personal Consumption Expenditures (PCE) report for October which saw both its headline and core rates continue to fall year-over-year.

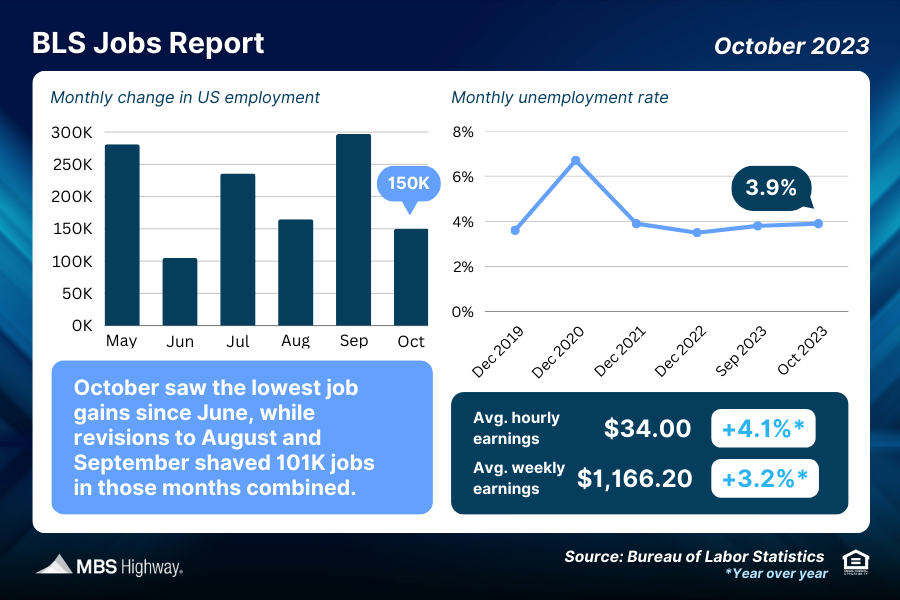

Moreover, a softer labor market with elevated unemployment and a reduction in job gains leads to a slowing of wage increases and less consumer spending. We are likely seeing the intended effects of the Federal Reserve (Fed) rate hikes take effect.

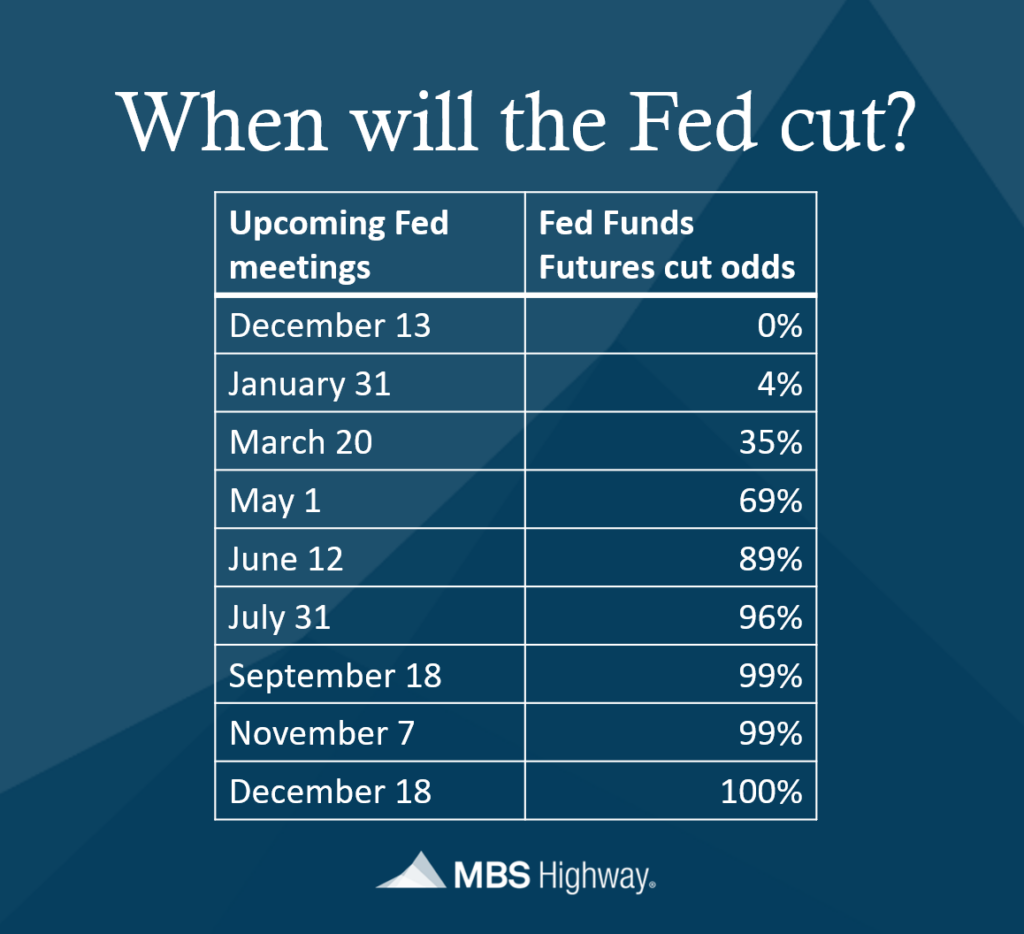

Where Are Rates Headed?

Recent trends we just discussed indicating lower inflationary pressures alongside a weakening job market have significantly increased the likelihood of a potential cut for the Fed Funds Rate cut in the coming six months. The diminishing inflation data, coupled with sluggish economic activity reflected in the softening job market, have increased expectations for the Fed to consider easing its monetary policy stance. A cut in the Fed Funds Rate becomes a tool to manage economic growth and inflation to maintain its 2% target.

As the Fed lowers interest rates or signals a more accommodative policy, it directly influences downward movement in mortgage rates. This is evident in the recent drop in rates throughout the month of November. With many leading indicators pointing towards a weakening economy and job market, we are likely to see this downward trend in rates continue into 2024.

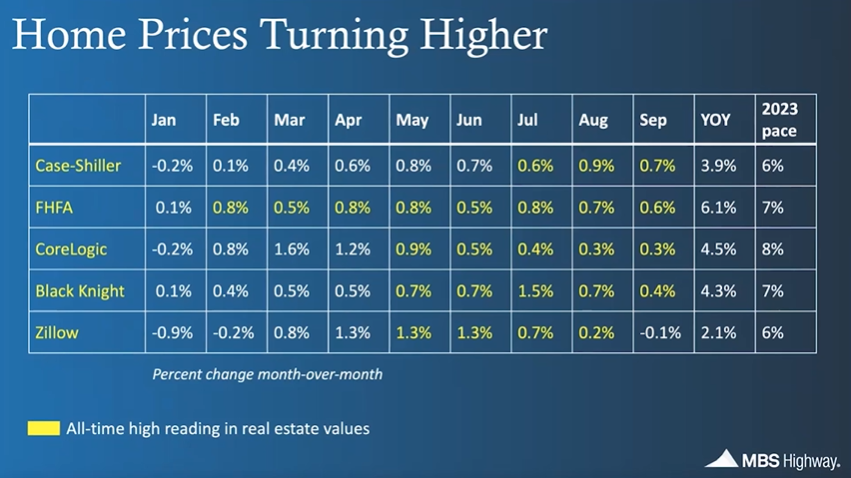

Home Values & Appreciation Trends

Amidst the current real estate landscape, home values continue to remain stable and exhibit consistent appreciation. In fact, five of the most notable home price indices highlight an annualized appreciation of 6% or higher through the end of 2023, underscoring the resilience and upward trajectory of property values. This has been primarily fueled by a shortage of home inventory. Forecasts for 2024 echo a continuation of this trend, as the imbalance between supply and demand remains a pivotal factor driving the market. The persistent shortage of available homes, compounded by a lag in housing starts failing to meet the pace of household formations, serves as a primary catalyst in the sustained appreciation of home values. This disparity between the growing demand for housing and the insufficient supply of available properties is anticipated to perpetuate the trend of appreciating home values well into the upcoming year where homeowners will gain significant equity.

The Current Window of Opportunity for Buyers

In the current winter market, a unique window of opportunity presents itself for prospective homebuyers, fueled by multiple favorable factors poised to shape the real estate landscape. Forecasts indicating an anticipated decline in mortgage rates set the stage for increased affordability, thereby widening the pool of potential buyers. As rates fall, accessibility to homeownership becomes more attainable, likely leading to heightened competition and subsequent upward pressure on home prices. Furthermore, the increase in new loan limits significantly contributes to affordability by granting buyers access to higher financing. Seizing this moment presents an advantage for buyers as purchasing now grants the advantage of entering the market ahead of the projected surge in competition. Moreover, buyers who secure properties during this time can capitalize on potential equity gains, with home values expected to appreciate into the upcoming year. Additionally, with the prospect of lower rates in the future, buyers have the option to refinance when rates decline further, maximizing financial benefits while ensuring a strategic investment in a burgeoning market. Hence, acting swiftly in the current market not only secures a foothold in less competitive conditions but also positions buyers to potentially gain from future equity growth and favorable refinancing opportunities.

When it comes to obtaining a mortgage for your dream home, Homeseed, an independent mortgage banker, is your go-to lender for a wide range of innovative loan programs strategies. As an independent mortgage banker, Homeseed offers correspondent, direct agency, and wholesale lending solutions, making it a one-stop-shop for all your mortgage needs. In addition to the standard conventional, government, and jumbo loan products, Homeseed provides a wide range of creative financing solutions and unique products designed to cater to your specific needs. In this post, we’ll take a closer look at the loan programs and strategies that many homebuyers are taking advantage of in today’s market and highlight all of the products offered by Homeseed.

Creative Financing Solutions

In a high-interest rate environment, securing an affordable mortgage becomes a paramount concern for prospective homebuyers. The importance of providing creative financing solutions cannot be overstated, as these solutions serve as a bridge between the desire for homeownership and the reality of higher interest rates. At Homeseed, we understand that clients should not be deterred from achieving their dream of homeownership due to market conditions and offer many financing solutions for clients to navigate these challenges effectively. Recently, homebuyers have found success using the following programs and strategies:

Down Payment Assistance Loans: These loans offer financial support that can help homebuyers cover the down payment requirements and closing costs.

DSCR (Debt Service Coverage Ratio) Loans: These loans are designed for real estate investors and focus on the rental income generated by the property to qualify for the mortgage. This is an excellent option for those wanting to get into real estate investment and even seasoned investors.

Temporary and Permanent Buydowns: Temporary and permanent buydowns offer clients the advantage of lower initial interest rates, lowering the monthly mortgage payments and making homeownership more accessible and affordable.

Buy Before You Sell Program: This program provides homeowners the flexibility to secure their new dream home before selling their current property, relieving the stress and need of having to submit a new offer with a contingency.

Construction/Renovation Loans: If you’re looking to build a custom home or purchased a discounted property that needs renovating, Homeseed offers construction and renovation loan options to help make your dream home a reality.

P&L (Profit and Loss) Loans: Homeseed offers loans that consider your business’s profit and loss statements, which can potentially help self-employed individuals and small business owners qualify for a higher purchase price on a home.

Bank Statement Loans: These loans use your bank statements to verify your income, making them an excellent choice for individuals with non-traditional income sources who also want to qualify more income for a higher home purchase price point.

HELOCs (Home Equity Line of Credit): Homeseed provides HELOCs that allow you to access the equity in your home for various purposes, such as home improvements, debt consolidation, or other financial needs while potentially allowing you to keep your primary fixed rate.

Ginnie Mae (FHA, VA, USD) seller-servicer & securitizer (direct bond market participant).

JUMBO LOANS

22 programs allowing 10% (or 10.01%) downpayment

Some programs allow 90% over $1.0M with <1 yr from a major credit event

40-yr mortgage & interest only options

10% downpayment on second homes

Lending with no max acreage limit

In-house delegated underwriting

RENOVATION LOANS

In-house funding & administration of FHA 203K, Fannie Mae Homestyle, and VA Renovation

Draws assisted and completed by Homeseed

CONSTRUCTION LOANS

In-house funding & administration of Conforming, FHA, VA, USDA & Jumbo construction loan.

0-5% downpayment options

Draws assisted and completed by Homeseed

DOWN PAYMENT ASSISTANCE

No income limit

Up to 5% assistance

Options for repayable and non-repayable assistance

Available on multi-family properties

OTHER LOAN PROGRAMS

Multiple programs that do 90% (or 89.99%) LTV on cash-out

DSCR: Investor cash flow

1099 Income Loan Program

Hobby farms: 5 programs including barndominiums and shouses

Raw land lending including farms

Agency & Non-agency manufactured homes

Programs for foreign national and ITIN borrowers

Multi-family and Fix & Flip programs (up to 25 units)

Programs that use 24- or 12- months bank statement for income (to 10% down)

Or use of previous year only income qualification

Use of stock units for income

Use of current financial assets to boost income for qualifying

For 2nd mortgages

Programs for non-warrantable condos (90% to $2.0M with 700)

Great programs with near-prime rates on condotels and non-warrantable condos

Multiple state & national down payment assistance programs

HELOCs & 2nd mortgages that can fund within a week, with a fee

*Information is subject to change without notice. This is not an offer for extension of credit or a commitment to lend. This ad is not from HUD, VA, or FHA and was not reviewed or approved by any government agencies.

Homeseed is now offering a Buy Before You Sell program for current homeowners who are looking to purchase a new residence. One of the main advantages is that it can provide flexibility and alleviate some of the stress homeowners face when purchasing a new home. The program allows homebuyers to move quickly on the purchase of the new home rather than worrying about selling their current residence. Additionally, it strengthens their offer on a new property as they are not contingent on the sale of their current home. This can be especially advantageous in a competitive real estate market, where buyers may face multiple offers on a property. Furthermore, this loan program can provide buyers with a bridge loan to help cover the down payment on the new purchase or to make repairs to the departing residence.

Get Started in Less Than 10 Minutes

Get pre-approved with our online mortgage application. It’s simple, fast & secure!